In yesterday’s double-dip “Emergency” budget, George Osborne announced a new tax that means that one group in society will be paying around £2,000 more from next April. No, it’s not hedge fund managers, multinationals or the ultra-rich. It’s small businesspeople.

A reform or just a tax-grab?

Sneaked in under the banner of ‘dividend taxation reform’, his tax hike on share dividends means people running their own businesses as limited companies and taking basic dividends will pay around £2,000 more tax next year.

How?

Taxing you twice

The Treasury used to believe that it was fair to tax things just once; apart from road fuel where drivers are made to pay Fuel Duty on the price of fuel then VAT on top of the Duty. It seems that enterprise is now fair game too.

If you run a small business, perhaps turning over £200,000 a year and employing a couple of people, you pay Corporation Tax at 20% on the profits. Business owners used to pay themselves using those profits (already taxed under Corporation Tax, remember) as dividends, paying no more tax until they hit the higher rate tax band.

Pay an extra £2,000 in tax – to start with

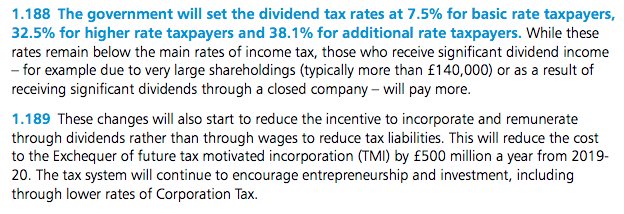

Let’s say, like most directors, you take some of your income in salary and some in dividends. As of next year, you’ll be paying an additional, new 7.5% Dividend Tax. Unless you earn enough to become a Higher Rate Taxpayer, in which case it’ll be an additional 32.5% of new tax.

For a pretty average business owner earning around £42,000, that’s going to be an extra £2,000 tax to pay on money that’s already been taxed once. And the Chancellor has made it very clear indeed that he sees this 7.5% tax raid as just the start. Expect to see it rise – sharply – in the next few years.

But it’s all OK because this “will continue to encourage entrepreneurship and investment, including through lower rates of corporation tax“. Let’s look at that…

Take the money now, get a bit back later

Reductions in Corporation Tax don’t start until two years later in 2017 (19%), then slowly phase in until 2019-20 (18%). The Dividend Tax hits straight and full-on from April ’17 on earnings from the previous tax year. And the dividend tax take has a rather greater impact on small businessmen’s income than the reductions in Corporation Tax. And, in the meantime, the Exchequer will see around £2.5bn in extra tax roll in.

“Aw, diddums,” you’re probably thinking. “£42k a year, your own business and bitching about paying a bit of extra tax”. Indeed. That’ll be £42k that’s come from someone leaving employment and starting their own business. No more company car, company pension scheme, lunch allowances, private healthcare, redundancy pay, sick pay or holiday pay. A lot of hours and a lot of stress, sweat and tears in the hope that they’ll – one day – make it. And most don’t.

Putting the brakes on enterprise

This is a raid on people who are starting out, perhaps a couple of years into running their own business and struggling to make it work. These are the businesses that are heading down the runway, building up speed and hoping to get properly off the ground.

Osborne said in his Budget:

“This is the first Conservative budget for 18 years. It was Conservatives who first protected working people in the mills, it was Conservatives who introduced state education, it was Conservatives who introduced equal votes for women. It was Conservatives that gave working people the Right to Buy, so of course it’s now the Conservatives who introduce the National Living Wage. For this is the party for the working people of Britain.”

He should have added “…unless they run their own businesses.”

Leave a comment